How Blockchain Is Changing Financial Services in 2026

The financial world is experiencing a seismic shift. After years of experimentation, blockchain in finance has moved from theoretical promise to practical reality. Banks that once dismissed distributed ledger technology are now racing to implement it. If you're a financial executive, fintech innovator, or simply curious about how blockchain is changing finance, this is your moment to pay attention.

In this guide, you'll discover why 2026 marks a critical turning point, how blockchain financial services are transforming traditional operations, and what this means for the future of finance and blockchain integration.

What Is Blockchain in Simple Terms

Think of blockchain as a shared record book that everyone in a network can view and verify, but no single person or company controls. Unlike traditional databases, a distributed ledger spreads information across multiple computers simultaneously.

Here's how blockchain works:

- Transparency: Transactions get recorded in blocks that link chronologically, creating an unchangeable chain of records.

- Security: Advanced cryptography protects each transaction, making tampering virtually impossible.

- Decentralization: No central authority controls the entire system, eliminating single points of failure.

- Verification: Network participants validate transactions through consensus mechanisms before they become permanent.

The distinction between public vs private blockchain matters tremendously in finance. Public blockchains like Bitcoin operate openly, while private blockchains restrict access to authorized participants, making them ideal for institutional use where privacy and compliance are paramount.

Why 2026 Is a Turning Point for Finance

Several forces are converging to make 2026 a watershed moment for blockchain adoption in financial services

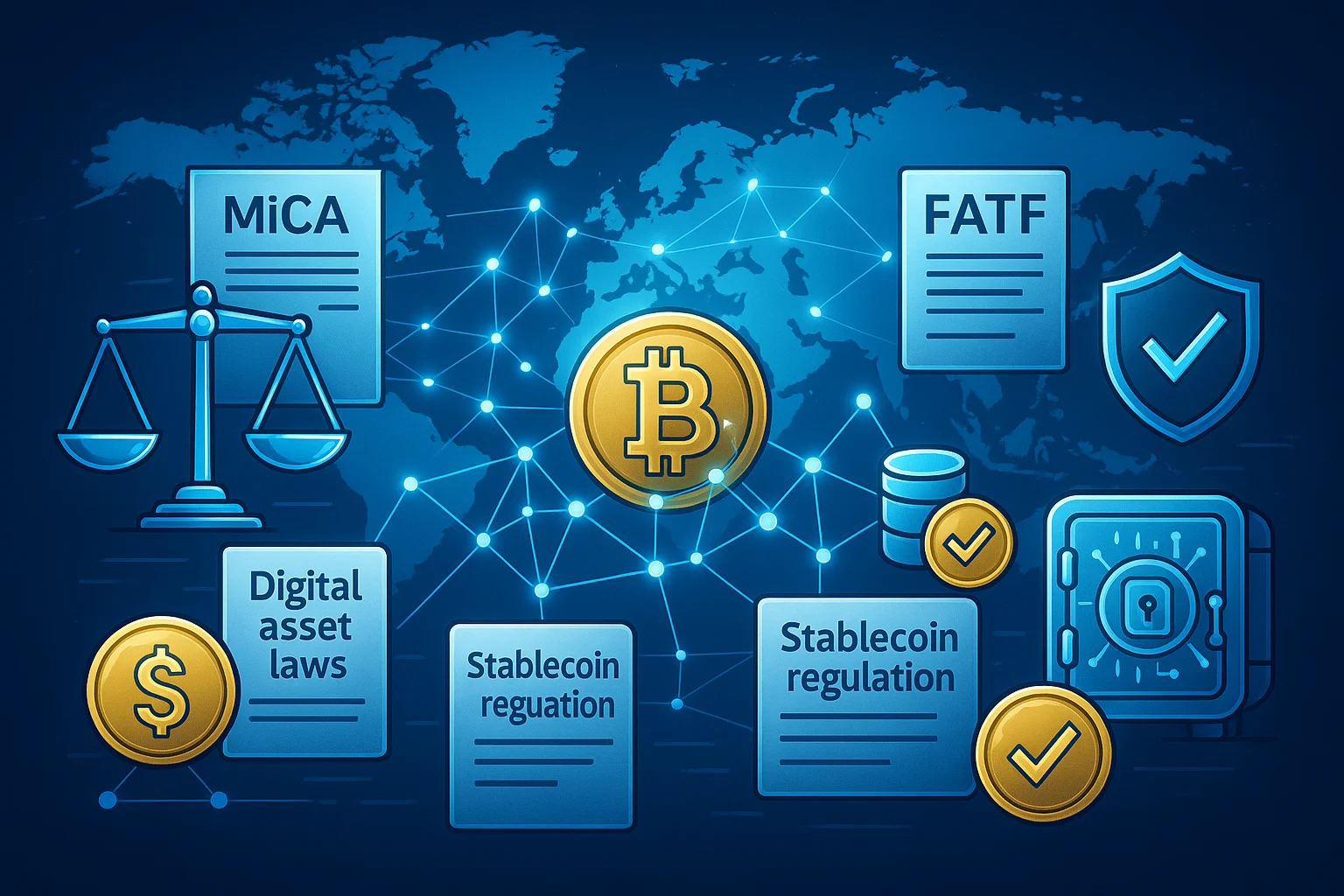

Regulatory Clarity Emerges

After years of uncertainty, blockchain regulation frameworks are solidifying globally. The European Union's MiCA regulation provides comprehensive rules for digital assets. The United States is moving toward clearer stablecoin regulation and securities guidelines. Asian markets have established regulatory sandboxes that encourage controlled innovation. This regulatory maturation gives financial institutions confidence to move beyond pilots into full production.

CBDC Developments Accelerate

CBDC developments represent perhaps the most significant shift in monetary systems in generations. Over 130 countries are exploring or piloting Central Bank Digital Currencies. The Digital Euro and Digital Dollar have concrete implementation timelines.

China's Digital Yuan has processed hundreds of billions in transactions. Brazil, India, and Australia are advancing programs rapidly. Wholesale CBDC initiatives are transforming interbank settlements, while retail variants promise to reshape consumer payments.

Tokenization Reaches Critical Mass

Asset tokenization has moved from niche experiments to mainstream adoption. The tokenization market shows exponential growth as billions in traditional assets convert to digital tokens. Real estate, bonds, equities, commodities, and art are being tokenized, creating fractional ownership opportunities.

This tokenization trend is unlocking trillions in previously inaccessible value. A $50 million property can now be divided into thousands of tokens, democratizing access.

Institutional Adoption Accelerates

Enterprise blockchain adoption statistics for 2026 show mainstream integration. Major banks, asset managers, and insurance companies are deploying production systems handling real money and assets.

Institutional blockchain adoption has crossed the chasm from early adopters to mainstream. Financial institutions recognize that blockchain adoption matters for both efficiency and competitive survival.

Major Ways Blockchain Is Transforming Financial Services

The blockchain impact on banking operations spans virtually every financial function. Here are the most significant blockchain use cases reshaping the industry.

Payments and Cross-Border Transfers

Traditionalcross-border payments are slow, expensive, and opaque. International wire transfers take days and cost $25 to $50 in fees, with multiple intermediaries taking cuts. Recipients often can't track their money or predict arrival times accurately.

Blockchain payments solve these problems elegantly:

- Transactions settle in minutes instead of days, with some networks completing transfers in seconds

- Costs drop to pennies instead of dollars, making micro-payments economically viable for the first time

- Complete transparency shows exactly where money is at every step of the journey

- 24/7 operation eliminates banking hour restrictions and holiday delays

- Reduced counterparty risk through automated settlement that doesn't require trust

Major institutions are already processing billions through blockchain payment networks, demonstrating that faster settlement blockchain isn't theoretical but operational.

Central Bank Digital Currencies

CBDCs represent government-issued digital currencies built on blockchain infrastructure. Unlike cryptocurrencies, CBDCs are legal tender backed by central banks.

The implications are profound:

- Programmable money enables conditional payments and automated compliance

- Real-time monetary policy implementation

- Financial inclusion for unbanked populations

- Reduced cash handling costs for governments

- Enhanced ability to track and prevent illicit finance

CBDC privacy concerns are being addressed through privacy-preserving technologies balancing transparency with individual rights. The digital currency race is accelerating as nations recognize strategic advantages.

Asset Tokenization and Securities

Securities settlement blockchain technology is revolutionizing capital markets. Traditional settlement takes two days (T+2) with numerous intermediaries. Blockchain enables instant settlement.

Real estate tokenization and fractional ownership platforms democratize access to high-value assets. A $10 million property can be divided into thousands of tokens.

Key benefits include:

- Dramatically improved liquidity for illiquid assets

- 24/7 trading without exchange hours

- Automated dividend distribution through smart contracts

- Reduced settlement risk and counterparty exposure

- Lower costs through disintermediation

Tokenization benefits are so compelling that Goldman Sachs, BlackRock, and Franklin Templeton are launching tokenization platforms for assets from bonds to commodities.

Trade Finance and Supply Chain

Trade finance blockchain applications address inefficiencies in international commerce. Letter of credit processes that required weeks now complete in hours.

Key improvements include:

- Digital documentation replacing paper-intensive processes

- Real-time shipment tracking and verification

- Automated payment release when conditions are met

- Reduced fraud through immutable record keeping

- Lower costs from eliminated intermediaries

Blockchain reduces the reconciliation burden by providing a single source of truth for all parties.

Lending and Credit

Smart contracts transform lending by automating processes that traditionally required manual underwriting.

Blockchain-enabled lending offers:

- Instant loan approval based on on-chain credit histories

- Automated collateral management and liquidation

- Transparent interest rate calculations

- Cross-border lending without currency conversion friction

- Institutional DeFi protocols offering competitive yields

Traditional banks are exploring hybrid models combiningblockchain for banking infrastructure with regulatory compliance.

Insurance

The insurance industry leverages blockchain to streamline claims processing and reduce fraud. Parametric insurance policies automatically pay out when predefined conditions are met.

Benefits include:

- Faster claims processing from weeks to minutes

- Reduced administrative overhead

- Enhanced fraud detection through data immutability

- Transparent policy terms and automated execution

- Lower premiums from efficiency gains

KYC and Compliance

KYC blockchain solutions address one of banking's most expensive processes. Customer identity verification currently happens separately at each institution, creating massive redundancy.

Blockchain for KYC and AML compliance enables:

- Shared digital identity verified once, accepted everywhere

- Secure credential sharing with customer consent

- Real-time sanctions screening and AML checks

- Reduced onboarding costs and time

- Better data privacy blockchain protections through encryption

Financial institutions implementing these systems report 50% reductions in compliance costs while improving accuracy.

Regulation and Compliance in 2025

The regulatory landscape for blockchain has matured significantly, moving from prohibition toward measured frameworks balancing innovation with protection.

Global Regulatory Developments

Crypto regulation varies by jurisdiction but shares common themes:

- MiCA regulation in Europe provides comprehensive rules for crypto assets, stablecoins, and service providers

- The FATF Travel Rule implementation requires cryptocurrency transfers to include sender and recipient information

- Stablecoin regulation is tightening globally, requiring reserves, audits, and banking-style oversight

- Digital asset laws are establishing clear classifications for tokens, securities, and commodities

Compliance Best Practices

Blockchain compliance best practices emphasize:

- Robust KYC and AML procedures integrated into blockchain systems

- Transaction monitoring and suspicious activity reporting

- Data protection complying with GDPR and similar frameworks

- Regular audits and third-party verification

- Regulatory sandbox participation to test innovations safely

RegTech blockchain solutions use distributed ledger technology to automate compliance reporting, making regulatory oversight more efficient.

The regulator guidance provided by authorities recognizes blockchain's benefits while establishing guardrails, enabling institutional blockchain deployment at scale.

Benefits for Financial Institutions

The blockchain benefits for banks extend beyond cost savings, though financial advantages are substantial.

Cost Efficiency

Blockchain cost savings come from multiple sources:

- Eliminated intermediaries reduce transaction fees

- Automated processes decrease labor costs

- Reduced reconciliation burden saves millions annually

- Lower compliance costs through automated reporting

- Decreased fraud losses from enhanced security

Industry estimates suggest blockchain financial services can make 30-70% cost reductions in back-office operations.

Speed and Efficiency

Faster settlement dramatically improves capital efficiency:

- Instant settlement reduces counterparty risk

- Real-time liquidity management

- 24/7 operations without banking hours

- Automated processes eliminate manual delays

Enhanced Security

Blockchain fraud reduction comes from inherent design features:

- Immutable records prevent tampering

- Cryptographic security protects transactions

- Distributed architecture eliminates single points of failure

- Transparent audit trails deter misconduct

Improved Liquidity

Blockchain improves liquidity through several mechanisms:

- Asset tokenization creates markets for illiquid holdings

- Instant settlement reduces locked capital

- Global access expands buyer pools

- Fractional ownership lowers entry barriers

Transparency and Trust

Blockchain transparency in finance builds confidence:

- All participants see identical records

- Audit trails provide complete transaction histories

- Smart contract automation eliminates execution disputes

- Regulatory compliance becomes verifiable

Challenges and Limitations

Despite tremendous progress,blockchain challenges remain that institutions must address thoughtfully.

Scalability Concerns

Blockchain scalability issues affect high-volume transaction processing. Public blockchains like Bitcoin process only 7 transactions per second, while Ethereum handles 30. Visa processes thousands per second.

Solutions include:

- Layer 2 scaling solutions that process transactions off-chain

- Private blockchain networks optimized for enterprise throughput

- New consensus mechanisms balancing security and speed

- Hybrid architectures combining blockchain with traditional systems

Addressing blockchain scalability issues in high-volume transactions is critical for mainstream adoption.

Interoperability Challenges

Blockchain interoperability remains fragmented, with different platforms unable to communicate seamlessly. Overcoming blockchain interoperability challenges for banks involves:

- Cross-chain bridges enabling asset transfers

- Standardized protocols and APIs

- Industry consortiums establishing common frameworks

- Middleware solutions translating between systems

Privacy and Security Concerns

Blockchain privacy concerns create tension between transparency and confidentiality. Financial institutions need privacy for competitive and regulatory reasons.

Solutions include:

- Zero-knowledge proofs that prove information without revealing it

- Private transactions on public chains

- Permissioned networks with access controls

- Encryption layers protecting sensitive data

Custody risks require robust solutions. mitigate custody risks for institutional digital assets demands enterprise-grade security infrastructure.

Legal and Regulatory Uncertainty

Legal challenges include unclear securities laws, cross-border jurisdiction questions, and smart contract enforceability. Regulatory uncertainty in blockchain slows deployment as institutions await clearer guidance.

Adoption Barriers

Adoption barriers include:

- Legacy system integration complexity

- Shortage of blockchain talent and expertise

- Cultural resistance to new technologies

- Need for industry-wide coordination

- Unclear business case for some applications

These limitations of blockchain in finance are surmountable but require sustained effort, investment, and collaboration.

Future Outlook: Where Blockchain Is Heading

The future of blockchain in finance looks increasingly integrated into mainstream infrastructure. Blockchain predictions suggest continued acceleration.

AI and Blockchain Convergence

Blockchain and AI integration for future financial services creates powerful synergies:

- AI analyzes blockchain data for fraud detection and risk assessment

- Smart contracts execute AI-driven decisions

- Decentralized AI training on blockchain-secured data

- Automated compliance using machine learning

AI-powered blockchain in finance applications will define competitive advantage in coming years.

Institutional DeFi Growth

Institutional DeFi involves traditional finance embracing decentralized protocols:

- Banks offering DeFi-powered products

- Tokenized treasury management

- Decentralized exchanges for institutional trading

- RWA tokenization bridging traditional and decentralized finance

Predictions for blockchain in the financial industry include seamless integration between centralized and decentralized systems.

Tokenization will become Standard

The Tokenization future suggests virtually all financial assets will exist in digital form:

- Securities issued as tokens by default

- Real estate and commodities routinely tokenized

- Fractional ownership standard across asset classes

- Digital assets future includes mainstream retirement accounts holding tokenized assets

Mainstream CBDC Adoption

CBDC future includes widespread retail and wholesale usage:

- Digital fiat replacing physical cash in many countries

- Cross-border CBDC networks enabling instant international settlement

- Programmable money enabling innovative financial products

- CBDC private sector collaboration creating public-private ecosystems

Strategic Implementation

Organizations should follow a blockchain adoption roadmap:

1.Education and stakeholder alignment

2.Pilot projects addressing specific pain points

3.Infrastructure development and system integration

4.Regulatory engagement and compliance building

5.Scaled deployment with continuous improvement

Top 3 blockchain trends to watch in 2026 and beyond include continued tokenization growth, CBDC implementation, and TradFi integration with decentralized protocols.

The strategic roadmap for blockchain implementation in finance requires long-term commitment but offers transformative competitive advantages.

Conclusion

Blockchain's impact on finance represents more than incremental improvement. It's a fundamental reimagining of how value moves, assets are owned, and trust is established in financial systems.

The technology has matured beyond hype to deliver measurable benefits:faster settlement, blockchain transparency, fraud reduction, and improved liquidity. Blockchain cost savings are proven, and the blockchain business case is increasingly compelling.

Yet challenges remain. Blockchain scalability, interoperability issues, regulatory uncertainty, and adoption barriers require ongoing attention and innovation. For financial institutions, the question is no longer whether to engage with blockchain but how quickly and strategically to implement it.